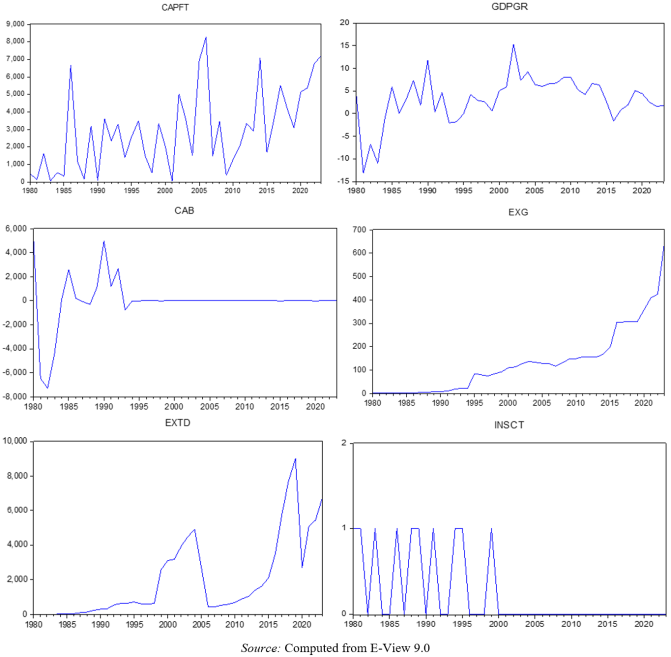

This study investigated the impact of capital flight on Nigeria’s economic growth from 1980 to 2023. Preliminary analyses, revealed that variables were stationary at level and first difference, I(0) and I(1), respectively. Given the data characteristics, the Autoregressive Distributed Lag (ARDL) bounds testing approach to cointegration was applied. The results from the ARDL model confirmed a significant long-run relationship between capital flight and economic growth, indicating an inverse relationship in both the short and long run. Specifically, external debt exerted a negative effect on growth in the short run (-0.94) but turned positive in the long run (-0.86). Insecurity, with coefficients (-1.06) and (-4.76), had a consistently negative and statistically significant impact on economic growth in both the short and long run. Similarly, the exchange rate negatively influenced growth in the short run (-0.02) but showed a positive long-run relationship (0.002). The current account balance, on the other hand, had a positive effect on economic growth in both the short run (0.0024) and the long run (0.0003). The Error Correction Model (ECM) reparameterization of the ARDL framework indicated a speed of adjustment of 95%, which was statistically significant and correctly signed, suggesting a strong tendency toward long-run equilibrium. Based on these findings, the study recommends that the Federal Government of Nigeria adopt comprehensive measures to curb the drivers of capital flight—such as macroeconomic instability, institutional weaknesses, and external incentives—through sound economic policies, political stability, and institutional strengthening. Furthermore, the government should intensify efforts to combat insecurity by equipping security agencies with modern technology and incentives, ensuring effective protection of lives, property, and the overall social, political, and economic development of the nation.

| Published in | Economics (Volume 15, Issue 2) |

| DOI | 10.11648/j.eco.20261502.11 |

| Page(s) | 29-40 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

Capital Flight, Current Account Balance, Economic Growth, Exchange Rate, External Debt, ARDL Model and Insecurity

GDPGR | CAPFT | EXTD | INSCT | EXG | CAB | |

|---|---|---|---|---|---|---|

Mean | 3.190055 | 2913.743 | 1958.245 | 0.227273 | 132.6170 | -23.54864 |

Median | 4.200375 | 2738.000 | 669.3250 | 0.000000 | 115.1250 | 2.980000 |

Maximum | 15.32920 | 8285.000 | 9022.420 | 1.000000 | 647.2700 | 5178.000 |

Minimum | -13.12800 | 5.000000 | 1.980000 | 0.000000 | 0.550000 | -7282.000 |

Std. Dev. | 5.162448 | 2288.920 | 2336.525 | 0.423915 | 141.2430 | 2061.113 |

Skewness | -0.930955 | 0.628509 | 1.347102 | 1.301583 | 1.538603 | -1.138488 |

Kurtosis | 5.167793 | 2.443315 | 3.935964 | 2.694118 | 5.585196 | 8.331699 |

Jarque-Bera | 14.97107 | 3.464988 | 14.91373 | 12.59506 | 29.61280 | 61.62133 |

Probability | 0.000561 | 0.176843 | 0.000577 | 0.001841 | 0.000000 | 0.000000 |

Sum | 140.3624 | 128204.7 | 86162.79 | 10.00000 | 5835.150 | -1036.140 |

Sum Sq. Dev. | 1145.987 | 2.25E+08 | 2.35E+08 | 7.727273 | 857832.4 | 1.83E+08 |

Observations | 44 | 44 | 44 | 44 | 44 | 44 |

Variables | ADF Statistics | Critical Value | P-Value | Order of Integration |

|---|---|---|---|---|

GDPGR | -3.7082 | -3.6010 (1%) -2.9350 (5%) -2.6058 (10%) | 0.0075 | I(0) |

lnCAPFT | -4.7976 | -3.5922 (1%) -2.9314 (5%) -2.6039 (10%) | 0.0003 | I(0) |

lnEXTD | -6.7348 | -3.5966 (1%) -2.9332 (5%) -2.6049 (10%) | 0.0000 | I(1) |

INSCT | -7.5032 | -3.6105 (1%) -2.9390 (5%) -2.6079 (10%) | 0.0000 | I(1) |

EXG | -5.2069 | -3.6056 (1%) -2.9369 (5%) -2.6069 (10%) | 0.0001 | I(1) |

CAB | -6.8283 | -3.6394 (1%) -2.9511 (5%) -2.6143 (10%) | 0.0000 | I(1) |

Null Hypothesis: No long-run relationships exist | ||

Test Statistic | Value | k |

F-statistic | 5.514790 | 5 |

Critical Value Bounds | ||

Significance | I0 Bound | I1 Bound |

10% | 2.26 | 3.35 |

5% | 2.62 | 3.79 |

2.5% | 2.96 | 4.18 |

1% | 3.41 | 4.68 |

Variables | Coefficient | Standard Error | T-statistics | Prob. |

|---|---|---|---|---|

C | 28.98130 | 9.501482 | 3.050188 | 0.0086 |

∆LnCAPFT(-1) | -2.194874 | 0.454690 | -4.827189 | 0.0003 |

∆LnEXTD | -0.935961 | 1.023351 | -0.914605 | 0.3759 |

∆INSCT | -1.670313 | 1.313347 | -1.271799 | 0.2242 |

∆EXG | -0.021745 | 0.013251 | -1.641036 | 0.1231 |

∆CAB | 0.002448 | 0.000636 | 3.848132 | 0.0018 |

ECMt-1 | -0.950108 | 0.178550 | -5.321255 | 0.0001 |

Variables | Coefficient | Standard Error | T-statistics | Prob. |

|---|---|---|---|---|

C | 30.503176 | 9.188051 | 3.319875 | 0.0051 |

Ln(CAPFT) | -3.984864 | 1.018669 | -3.911836 | 0.0016 |

Ln(EXTD) | 0.857580 | 0.551711 | 1.554400 | 0.1424 |

INSCT | -4.761765 | 4.091616 | -1.163786 | 0.2640 |

EXG | 0.002413 | 0.010263 | 0.235130 | 0.8175 |

CAB | 0.000310 | 0.000830 | 0.373818 | 0.7141 |

F-statistic | 0.553264 | Prob. F(25,14) | 0.9046 |

Obs*R-squared | 19.87898 | Prob. Chi-Square(25) | 0.7531 |

Scaled explained SS | 1.794004 | Prob. Chi-Square(25) | 1.0000 |

ARDL | Autoregressive Distributed Lag |

CAPFT | Capital Flight |

CAB | Current Account Balance |

EXR | Exchange Rate |

ECM | Error Correction Mechanism |

FDI | Foreign Direct Investment |

GCF | Gross Capital Formation |

GDPGR | Gross Domestic Product Growth Rate |

INSCT | Insecurity |

IMF | International Monetary Fund |

Ln | Log Linear |

OLS | Ordinary Least Squares |

| [1] | Adedayo, O. C. & Ayodele, S. O. (2016). An empirical analysis of the impact of capital flight on Nigeria economy. International Journal of Academic Research in Economics and Management Sciences 5(2), 2226-3624. |

| [2] | Adekunle, A. (2011). An economic analysis of capital flight from Nigeria. Policy Research Working Papers, Country Operations. World Bank WPS 993A. |

| [3] | Ajayi, S. I. (2003). An analysis of external debt and capital flight in the severely indebted low income countries in Sub-Saharan Africa, Research Department, International Monetary Fund Working Paper 68 (Washington DC). |

| [4] | Ajayi, S. I. (1995). Capital flight and external debt in Nigeria. African Economic Research Consortium (AERC) 10(1), 1-40. Research Paper 35. |

| [5] | Ajayi, L. B. (2012). Capital flight and Nigeria economic growth. Asian Journal of Finance and Accounting, 4(2), 277-289. |

| [6] |

Alabi, O. R. & Ogboru, I. (2019). Effects of capital flight on exchange rate in Nigeria: 1986-2015. RAIS Journal for Social Sciences. 3(1), 15.

https://doi.org/10.5281/zenodo.3066451 Retrieved on Oct. 22nd, 2021. |

| [7] | Amos O. A. & Obansa, S. A. J. (2025): “The Effect of Foreign Direct Investment on the Growth of Nigeria Economy. (A Case of Manufacturing Sector: 1980-2023”). Being a Research article published from Journal of Economics, Innovative Management and Entrepreneurship on |

| [8] | Asongu, S. (2014). Fighting African capital flight: Empirics on Benchmarking Policy Harmonization. JEL: C50; E62; F34; O19; O55. |

| [9] |

Attah-Obeng, P. En, P. Osei-Gyimah, F. & Opoku, C. D. K. (2013). An Econometric analysis of relationship between GDP growth rate and exchange rate in Ghana. Journal of Economics and Sustainable Development, 4(9).

https://www.jitse./org/journals/index.php/JEDS/article/view/6473 |

| [10] | Bonilla, R. (2004). Macroeconomic Policy, Structural Adjustment and Debt Relief, International Development Research Centre (IDRC), Document 4. |

| [11] |

Busari, E. (2010). Capital flight and Nigeria’s economy. Journal of Economic Development, 10(2), 304-320. Retrieved from

http://www.ajol.info/journals/jorind on 24/01/22. |

| [12] |

Cuddington, F. (1986). Capital flight: Estimates, issues and explanations. Princeton Studies International Finance. 58(2), 17-18. Retrieved from

https://ies.princeton.edu/pdf/S58.pdf on 14/12/21 |

| [13] | Erdoğdu H. and Çǐçek H. (2017). Modelling beef consumption in Turkey: the ARDL/bounds test approach. Turkish Journal of Veterinary and Animal Sciences. 41: 255-264. Retrieved from |

| [14] |

Egbuwalo, M. O. & Abere, B. O. (2018). Capital Flight and the Growth of Nigerian Economy: An Autoregressive Distributed Lag (ARDL) Modeling. IIARD International Journal of Economics and Business Management 4(2). Retrieved on from

https://www.ijardjournals.org/get/IJEBM/VOL.%204%20NO.%202%202018/CAPITAL%20FLIGHT.pdf on 14/12/21 |

| [15] | Kolapo, F. T., & Oke, M. O. (2012). Nigerian economic growth and capital flight determinants. Asian Journal of Business and Management Sciences, 1(11), 76-84. |

| [16] | Kingsley, O. O. & Eberechi, B. N. (2016). Influence of capital flight on budget implementation in Nigeria. Scientific Paper Serves Management, Economic Engineering in Agriculture and Rural Development. 16(4), 247-256. |

| [17] | Lawal, A. I., Kazi, P. K., Adeoti, O. J., Osuma, G. O. Akinmulegun, S. & Ilo, B. (2017). Capital flight and the economic growth: Evidence from Nigeria. Binus Business Review, 8(2), 125-132 |

| [18] | Mahon, J. E. (1996). Mobile capital and Latin America. Latin America Department. Pennsylvania University Press. |

| [19] | Makwe, E. U. & Oboro, O. G. (2019). Capital flight and economic growth in Nigeria. International Journal of Business and Management Review 7(8), 47-76, Published by ECRTD-UK. |

| [20] | Massa, I. (2014). Capital flight and the financial system. Working paper 413. |

| [21] | National Bureau of Statistics, (2016). National economic construction fund. (NERFUND). Abuja: NBS. |

| [22] | National Bureau of Statistics, (2020). Annual Abstract of Statistics. Abuja: NBS. |

| [23] | Ndikumana, L. (2014). Savings, capital flight, and African development. Research in Economics and International Finance. Working Paper Series from Political Economy Research Institute, number 351. Retrieved from |

| [24] | Nelson, J. Krokeme, O. Markjarkson, D. & Timipere, E. T. (2018). Impact of capital flight on exchange rate in Nigeria. International Journal of Academic Research in Accounting, Finance and Management Sciences, 8(1), 41–50, © 2018 HRMARS |

| [25] | Ojonugwa, A. E. & Musa, L. P. (2019). Impact of real exchange on economic growth. DUTSE Journal of Economics and development Studies. 7(1), 22-31. |

| [26] | Oladimeji, J. A., Adebayo, O. O., and Ohiaeri, N. V. (2022). The growth impact of capital flight in Nigeria. International Journal of Social Science and Economic Research. 7(3). 694-715. |

| [27] | Olatunji, O. & Oloye, M. I. (2015). Impacts of capital flight on economic growth. International Journal for Innovation Education and Research, 3(8), 407. Retrieved from |

| [28] | Olawale, O. & Ifedayo, O. M. (2015). Impacts of capital flight on economic growth in Nigeria. International Journal for Innovation Education and Research, 3(8), 12-25. |

| [29] | Orji, A., Ogbuabor, J. E., Kama, K., and Anthony-Orji, O. I. (2020). Capital Flight and Economic Growth in Nigeria: A New Evidence from ARDL Approach. Asian Development Policy Review, 8(3), 171–184. |

| [30] | Onyele, K. O. & Nwokocha, E. B. (2016a). The relationship between capital flight and poverty: The case of Nigeria. Scientific Papers Series Management, Economic Engineering in Agriculture and Rural Development, 16(3), 15-24. |

| [31] | Otene, S. (2010). The impact of capital flight on economic growth in Nigeria. Department of Economics, University of Nigeria, Nssukka Published M.Sc. Thesis. |

| [32] | Rosenje, M. O. & Adeniyi, O. P. (2022). The impact of banditry on Nigeria’s security in the fourth republic: An evaluation of Nigeria’s northwest. September, 2022. Retrieved 29th Dec., 2022 from |

| [33] | Saheed, Z. S. & Ayodeji, S. (2012). Impact of capital flight on exchange rate and economic growth in Nigeria. International Journal of Humanities and Social Science 2(13), 247-255. Retrieved 20 August, 2021 from |

| [34] |

Sami, A. K. & Mbah, S. A. (2018). External debt and economic growth: a case of emerging economy. Journal of Economic Integration, 33(1), 1141-1157.

http://dx.doi.org/10.11130/jei.2018.33.11141 on 20/12/21. |

| [35] | Schneider, B. (2003). Measuring Capital Flight: Estimates and Interpretations. Overseas Development Institute Working Paper 194. |

| [36] | Todaro, P. M. & Smith, C. S. (2009). Economic development. Pearson Education Limited Delhi 110092, India. |

| [37] | Uguru, L. C. (2016). On the tax implications of capital flight: Evidence from Nigeria. Journal of Research in Economics and International Finance (JREIF) (ISSN: 2315-5671) 5(1), 001-007. |

| [38] | Ugwuanyi, B. U. & Onyeka, V. N. (2012). Foreign exchange volatility and economic growth in Nigeria. ESUT Journal of Accountancy, 3(1), 118-124. |

| [39] | World Bank (1985). Case study: Mexico. In Lessard D. R. and Williamson, J. (eds.). Capital Flight and Third World Debt. Washington D.C: Institute of International Economics. |

APA Style

Amos, O. B. A., Obansa, S. A. J. (2026). Capital Flight and Growth of Nigeria’s Economy (1980-2023): An Autoregressive Distributed Lag (ARDL) Modelling. Economics, 15(2), 29-40. https://doi.org/10.11648/j.eco.20261502.11

ACS Style

Amos, O. B. A.; Obansa, S. A. J. Capital Flight and Growth of Nigeria’s Economy (1980-2023): An Autoregressive Distributed Lag (ARDL) Modelling. Economics. 2026, 15(2), 29-40. doi: 10.11648/j.eco.20261502.11

@article{10.11648/j.eco.20261502.11,

author = {Oluwafemi Benjamin Adeyemi Amos and Sumaila Adavani Joseph Obansa},

title = {Capital Flight and Growth of Nigeria’s Economy (1980-2023): An Autoregressive Distributed Lag (ARDL) Modelling},

journal = {Economics},

volume = {15},

number = {2},

pages = {29-40},

doi = {10.11648/j.eco.20261502.11},

url = {https://doi.org/10.11648/j.eco.20261502.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.eco.20261502.11},

abstract = {This study investigated the impact of capital flight on Nigeria’s economic growth from 1980 to 2023. Preliminary analyses, revealed that variables were stationary at level and first difference, I(0) and I(1), respectively. Given the data characteristics, the Autoregressive Distributed Lag (ARDL) bounds testing approach to cointegration was applied. The results from the ARDL model confirmed a significant long-run relationship between capital flight and economic growth, indicating an inverse relationship in both the short and long run. Specifically, external debt exerted a negative effect on growth in the short run (-0.94) but turned positive in the long run (-0.86). Insecurity, with coefficients (-1.06) and (-4.76), had a consistently negative and statistically significant impact on economic growth in both the short and long run. Similarly, the exchange rate negatively influenced growth in the short run (-0.02) but showed a positive long-run relationship (0.002). The current account balance, on the other hand, had a positive effect on economic growth in both the short run (0.0024) and the long run (0.0003). The Error Correction Model (ECM) reparameterization of the ARDL framework indicated a speed of adjustment of 95%, which was statistically significant and correctly signed, suggesting a strong tendency toward long-run equilibrium. Based on these findings, the study recommends that the Federal Government of Nigeria adopt comprehensive measures to curb the drivers of capital flight—such as macroeconomic instability, institutional weaknesses, and external incentives—through sound economic policies, political stability, and institutional strengthening. Furthermore, the government should intensify efforts to combat insecurity by equipping security agencies with modern technology and incentives, ensuring effective protection of lives, property, and the overall social, political, and economic development of the nation.},

year = {2026}

}

TY - JOUR T1 - Capital Flight and Growth of Nigeria’s Economy (1980-2023): An Autoregressive Distributed Lag (ARDL) Modelling AU - Oluwafemi Benjamin Adeyemi Amos AU - Sumaila Adavani Joseph Obansa Y1 - 2026/04/23 PY - 2026 N1 - https://doi.org/10.11648/j.eco.20261502.11 DO - 10.11648/j.eco.20261502.11 T2 - Economics JF - Economics JO - Economics SP - 29 EP - 40 PB - Science Publishing Group SN - 2376-6603 UR - https://doi.org/10.11648/j.eco.20261502.11 AB - This study investigated the impact of capital flight on Nigeria’s economic growth from 1980 to 2023. Preliminary analyses, revealed that variables were stationary at level and first difference, I(0) and I(1), respectively. Given the data characteristics, the Autoregressive Distributed Lag (ARDL) bounds testing approach to cointegration was applied. The results from the ARDL model confirmed a significant long-run relationship between capital flight and economic growth, indicating an inverse relationship in both the short and long run. Specifically, external debt exerted a negative effect on growth in the short run (-0.94) but turned positive in the long run (-0.86). Insecurity, with coefficients (-1.06) and (-4.76), had a consistently negative and statistically significant impact on economic growth in both the short and long run. Similarly, the exchange rate negatively influenced growth in the short run (-0.02) but showed a positive long-run relationship (0.002). The current account balance, on the other hand, had a positive effect on economic growth in both the short run (0.0024) and the long run (0.0003). The Error Correction Model (ECM) reparameterization of the ARDL framework indicated a speed of adjustment of 95%, which was statistically significant and correctly signed, suggesting a strong tendency toward long-run equilibrium. Based on these findings, the study recommends that the Federal Government of Nigeria adopt comprehensive measures to curb the drivers of capital flight—such as macroeconomic instability, institutional weaknesses, and external incentives—through sound economic policies, political stability, and institutional strengthening. Furthermore, the government should intensify efforts to combat insecurity by equipping security agencies with modern technology and incentives, ensuring effective protection of lives, property, and the overall social, political, and economic development of the nation. VL - 15 IS - 2 ER -

Department of Economics, University of Abuja, Abuja, Nigeria

Research Fields: Macroeconomics, Labour Economics, Mathematical Economics, Statistics Economics, International Economics, and Econometrics

Department of Economics, University of Abuja, Abuja, Nigeria

Research Fields: Health Economics, Macroeconomics, Statistics Economics, Mathematical Economics, Quantitative Economic Analysis, Industrial Economics, and Econometrics

Information